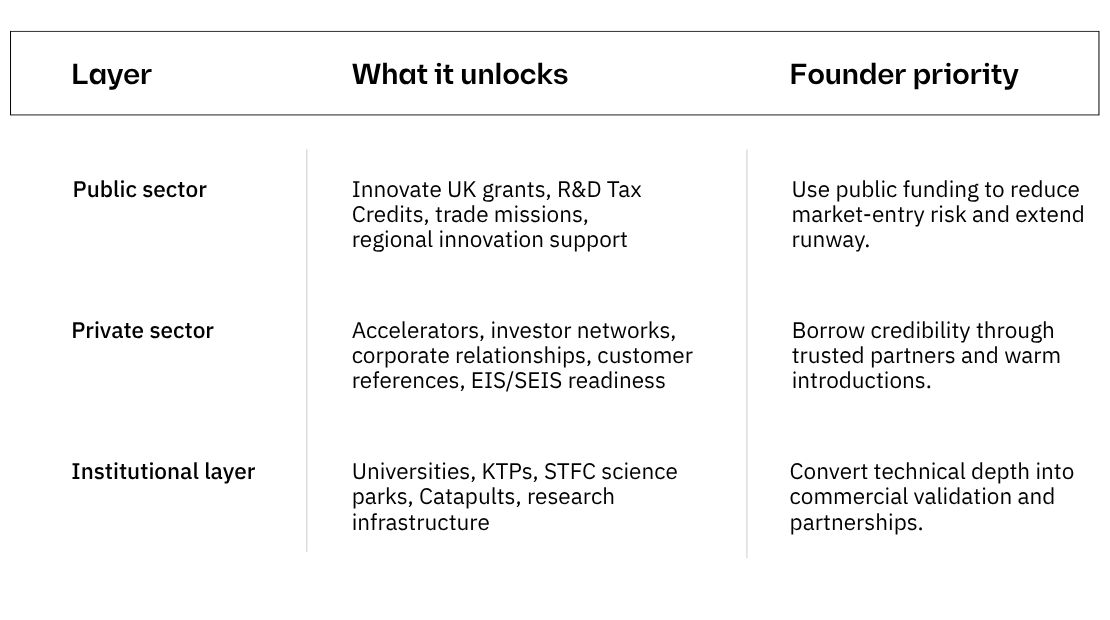

Highly useful when the company is already doing R&D and can manage applications and reporting. Innovate UK grants, R&D Tax Credits, KTPs, and regional support can extend runway without dilution.

The UK as Europe’s AI Capital: A Market Entry Playbook for International Founders

The UK is no longer simply a strong European expansion option. It is becoming a proving ground for AI-enabled companies, fintech infrastructure, public-private R&D, and trust-based B2B growth. The opportunity is real, but the market rewards founders who enter with focus, credibility, and a clear sequence.

The signal founders should not ignore

In Q1 2026, UK venture capital reached $7.8B, with $5.8B flowing into AI startups. That means AI captured 74% of UK VC in one quarter. The UK also attracted 41% of all European VC, more than France, Germany, and the Netherlands combined.

For Tenity, the strategic implication is clear: the UK is not only a funding market. It is a market where technology companies can validate whether their proposition is credible enough for sophisticated investors, regulated customers, corporate buyers, and institutional partners.

- The UK offers one of Europe’s strongest combinations of capital, AI momentum, fintech depth, corporate access, and public-sector R&D support.

- AI dominance is changing the standard for every sector. Fintech, health tech, deep tech, and SaaS companies need meaningful AI integration, not surface-level positioning.

- Market entry is primarily a trust challenge. Warm introductions, accelerators, reference customers, expert communities, and institutional partners create the credibility that cold outreach cannot.

- Non-dilutive funding can materially extend runway, but only for companies that structure their UK presence and R&D roadmap correctly.

- The best UK expansion plans start narrow: one customer segment, one traction goal, one decision maker, and one credibility strategy.

The Tenity perspective: why the UK matters now

At Tenity, we see market access as more than geographic expansion. For international founders, entering the UK is a test of strategic discipline: can the company translate traction from its home market into a new ecosystem with different buyers, funding logic, regulatory expectations, and trust dynamics?

Capital is active, AI investment is concentrated, fintech infrastructure is mature, and public-sector support remains meaningful. But founders should not mistake market attractiveness for market ease. The UK rewards clear relevance, targeted positioning, and local credibility.

AI is the market entry filter

The UK’s AI investment surge is not only relevant for AI-native companies. It is reshaping expectations across sectors. Investors and enterprise buyers increasingly look for AI that improves workflow efficiency, decision quality, risk assessment, customer experience, compliance, or cost structure.

For founders, the question is not whether AI appears in the pitch deck. It is whether AI creates a defensible advantage in the product, business model, or go-to-market strategy.

How the UK ecosystem actually works

The go-to-market mistake: assuming trust travels

Many founders enter the UK with a playbook that worked at home: familiar messaging, familiar channels, familiar assumptions about buyer trust. The problem is that trust rarely transfers automatically. In the UK, especially in B2B and regulated sectors, credibility is built through relevance, local proof, and repeated exposure within the right networks.

Before scaling marketing spend, founders should validate the UK-specific ICP, test positioning with small experiments, and build a focused group of early advocates. In many cases, curated dinners, expert roundtables, customer-led sessions, and partner introductions outperform broad paid campaigns because they create trust before asking for conversion.

A practical UK market-entry sequence

- Define one UK ICP. Identify the exact buyer, budget owner, pain point, trigger event, trusted information channels, and buying process.

- Test before scaling. Validate messaging and acquisition channels with small experiments before committing major budget.

- Build proof with a focused audience. Prioritise 100 to 200 high-fit prospects, early users, or ecosystem advocates before broadening reach.

- Use credibility-based formats. Warm introductions, expert communities, accelerators, customer references, and curated events can shorten the trust-building cycle.

- Scale after signal. Increase spending only when there is evidence of repeatable buyer interest, conversion, and messaging-market fit.

London is the entry point, not the whole strategy

London remains the natural starting point for many international founders because it concentrates investors, corporates, fintech infrastructure, talent, and global visibility. But the strongest UK strategy may also include Oxford, Cambridge, Manchester, Leeds, Edinburgh, Daresbury, or Harwell.

R&D-heavy companies should consider the Golden Triangle, science parks, and Catapult networks. The right location is where the company can access customers, talent, infrastructure, and credibility fastest.

Founder checklist before entering the UK

- Customer segment: Which single UK buyer group will you target first?

- Traction goal: What does success mean in the next 6 to 12 months: LOIs, pilots, ARR, partnerships, regulatory progress, or fundraising?

- Decision maker: Who signs, who influences, and who can block the deal?

- Funding path: Will expansion be led by grants, angels, VC, corporate partnerships, or revenue?

- Credibility strategy: Which partners, programmes, communities, and reference customers will help you earn trust?

- AI narrative: How does AI create measurable value in the product or business model?

The UK is one of Europe’s most compelling markets for AI-enabled and technology-driven companies. But entering successfully requires more than ambition. Founders need disciplined focus, local credibility, and a sequenced approach to funding, customers, regulation, and partnerships.

The UK should be treated as a strategic market access opportunity, not a generic expansion checkbox. The winners will enter early enough to benefit from momentum, but thoughtfully enough to earn trust.

FAQ for international founders

How useful are grants and non-dilutive funding?

Should fintechs wait for full FCA approval before building visibility?

No. Founders can build credibility in parallel through ecosystem participation, expert content, informational customer conversations, and warm introductions. Product claims and sales activity must stay aligned with regulatory status.

What is the best route for raising from angels with SEIS eligibility?

Start with SEIS-active angels whose sector, stage, and ticket size match the company. Combine targeted investor mapping with platforms and networks where investors already understand SEIS.

How should deep tech founders move from research to commercialisation?

Use university commercialization teams, STFC science parks, KTPs, and UK Catapults to access technical infrastructure, corporate partners, and commercial validation.

What is the biggest challenge for international founders?

The biggest challenge is not incorporation. It is trust. The founders who move fastest build relationships before selling and use credible partners to open the right doors.